According to an informal survey of a number of senior industry professionals, the semiconductor industry is at a turning point from now to the next few years. Start-up fabless semiconductor companies can get 100 million to 200 million US dollars of funds to develop a new generation of complex system single-chip (SoC) products, the time has passed. Venture capitalists did not receive equal returns on their investments, and partners who had advocated aggressive investments in the past had long left the industry.

According to an informal survey of a number of senior industry professionals, the semiconductor industry is at a turning point from now to the next few years. Start-up fabless semiconductor companies can get 100 million to 200 million US dollars of funds to develop a new generation of complex system single-chip (SoC) products, the time has passed. Venture capitalists did not receive equal returns on their investments, and partners who had advocated aggressive investments in the past had long left the industry. So where do you go next? Will there be more semiconductor startups? How will they receive funding? How can we achieve breakthrough innovation in a severely restricted fundraising environment?

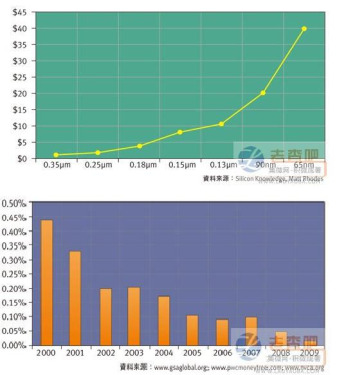

To understand the plight of the industry, we must consider the difference between IC development costs (Figure 1) and the startup's previous investment trend line (Figure 2). After interviews with more than 25 stakeholders in the industry, including venture capitalists, founding CEOs of semiconductor companies, and CEOs of start-up companies, we came to the conclusion that emerging trends may lead to semiconductors. The industry has changed from a dynamic technology and economic innovation engine to an underwriter who can only provide 'Me too' products.

Figure 1: Cost of developing integrated circuits per unit process (in millions of US dollars).

From this interview, we have identified three major trends. First of all, smaller players consolidation is accelerating for larger companies. In fact, over the past decade, many companies have retired from the semiconductor industry through mergers and acquisitions; IPOs have virtually disappeared. Even medium-sized listed companies have experienced substantial consolidation over the past few years. Second, companies that are backed by venture capitalists and have raised new funds are focused on specific niche markets. For example, some manufacturers develop proprietary analog and mixed-signal ICs; these components usually have larger process geometries and relatively low integration, which will enable the industry to maintain a reasonable cost. Finally, the activities of the new entrepreneurs at SoC seem to have calmed down, because the development of these highly complex components requires extremely large costs.

So what's left of this industry? Quite regrettable, for entrepreneurs, the only remaining ones may be more and more narrow space and less capital investment. However, new start-ups may still have a place in this industry, perhaps focusing on certain small markets with limited growth potential; or making themselves an IP supplier, following the ARM and MIPS models. Both of these conditions provide a very impressive financial performance, which in turn adds vitality to the venture capital industry.

In the interview, a senior CEO pointed out that the chip industry may look more and more like the automotive industry - mature, slow progress, and dominated by a few large companies. Other industry sources believe that the model adopted by the pharmaceutical industry can prevail; some small companies in the development stage have created intellectual property rights with great potential, and then sell it to large companies with a lot of resources to promote the market. In addition, an interviewee pointed out that the industry may return to the times dominated by large-scale laboratories, such as Bell Labs, Xeror Parc, and Sarnoff. However, in any of the above situations, there is no room for venture capitalists to invest in capital, and there is no room for real breakthrough technology.

Is it inevitable that our industry will continue to mature to marginalization? Or is there still other possibilities?

Recalling the successful example of a recent wave of new semiconductor entrepreneurs, Broadcom and Marvell are two good examples. The two companies founded in the 1990s have made significant achievements in the past decade. There are two main factors that contribute to their success in the market.

First, both companies adopt a pure fabless semiconductor company operating model. This strategy frees them from huge investments, otherwise they will always be committed to building huge production facilities. More efficient use of capital is necessary. However, for this industry, success is often accompanied by disruptive innovations.

Companies with destructive innovation traits, such as Broadcom and Marvell, have brought to the market a combination of system developers (including communications system engineers and scientists) and IC circuit developers - these talents are all for SoC development. Short. Almost every semiconductor industry expert who spoke to us emphasized that they now have far more software developers than IC designers. This change is the result of innovation brought directly to the industry by SoC designers.

Now, these companies are about to introduce innovative SoC thinking to the market, no longer limited to disruptive innovations. These companies now emphasize continuous innovation. Yes, they bring new thinking and updated system technologies to the silicon industry, and existing SoC operators already have the ability to do so.

When Broadcom and Marvell entered the market, the semiconductor industry that dominated the market had not hired engineers who could design innovative adaptive filters or complex modems and Reed-Solomon codecs. At the time, this was the work of system OEMs. But now, almost all semiconductor companies have system engineers and developers; due to the rising cost of development, having these engineering personnel is even more advantageous.

From this perspective, it seems unreasonable to try to invest in SoC startups. We can not help but ask what is the symbol of disruptive innovation in the semiconductor field. SoC last game, not the next one.

The industry executives who spoke to us agreed that the semiconductor industry still has the need for innovation. They cited increasing bandwidth requirements for communications and consumer electronics; the demand for lighter, more efficient power supplies for mobile devices and cars, and new energy solutions that can deliver energy to consumers and corporate clients in a smarter way. . But they also believe that to truly meet these needs, the existing technology layout still lacks some key points.

So, do they think that the wave of semiconductor startups is likely to come back?

In our interview survey, some respondents believe that 'chipless' semiconductor companies may become future industry pioneers such as eSilicon and Global Unichip. The move to 'chipless' will significantly reduce the upfront investment costs required to bring new semiconductor products to market.

Some CEOs stated that the upsurge of integrating sensors and drivers into semiconductor components is continuing and is expected to become a major driving force driving the development of semiconductors toward higher levels of integration. The ability to add components such as gyroscopes, accelerometers, camera parts, microphones, and magnetometers to the chip will be key, especially if standard CMOS processes are used. These capabilities will be groundbreaking.

In fact, micro-electromechanical systems (MEMS) have elevated the level of chip integration to a new level, which is expected to bring the next wave of large-scale disruptive innovations to the semiconductor industry.

No one can predict when the next wave of semiconductor transitions will occur. However, based on past industrial experience, as long as one person does the right thing and realizes technological innovation and breakthroughs, it is likely to drive the next wave of innovation.

Can the semiconductor industry regain the enthusiasm, vitality, and energy that it had previously had? The answer will depend on whether entrepreneurs make the right decision for innovation.

We are at a turning point in the chip industry. For the semiconductor industry, whether it is innovation or continuous consolidation and cost reduction, these trends may become more and more common in countries outside the United States.

Figure 2: Percentage of chip industry revenue for the first round of investment in the semiconductor industry.

This article was written by Bruce Kimble, Marty McMahon, and Matt Rhodes, three semiconductor industry experts. Kimble is an expert in the semiconductor industry; McMahon is an expert in the clean energy industry and works for McDermott & Bull, a research company in California; Rhodes is a long-term investor in the semiconductor industry.

Haoshuo Technology Co., Ltd. , http://www.whrollformingmachine.com